.png)

Deciding whether to renovate your current home or move to a new one is one of the most financially and emotionally significant choices homeowners face. Each path carries its own risks, rewards, and hidden costs, both practical and personal.

The right decision balances lifestyle needs, budget, location priorities, and the true potential of your current property.

For many homeowners, emotion drives the first impulse: the memories, neighbors, and community ties that make a house feel like home. Yet the most effective decisions weigh those emotional anchors against long-term financial logic.

If your neighborhood is appreciating, renovation often compounds value. But if nearby homes are stagnant or new developments outpace your area, investing more money in an underperforming market can be a losing proposition.

Conversely, relocating may provide access to better schools, shorter commutes, and lifestyle upgrades that renovation alone can’t deliver.

Renovation works best when your current home still aligns with your future goals — but simply needs updates or optimization. Typical cases include growing families, energy-efficiency upgrades, or modernizing outdated layouts.

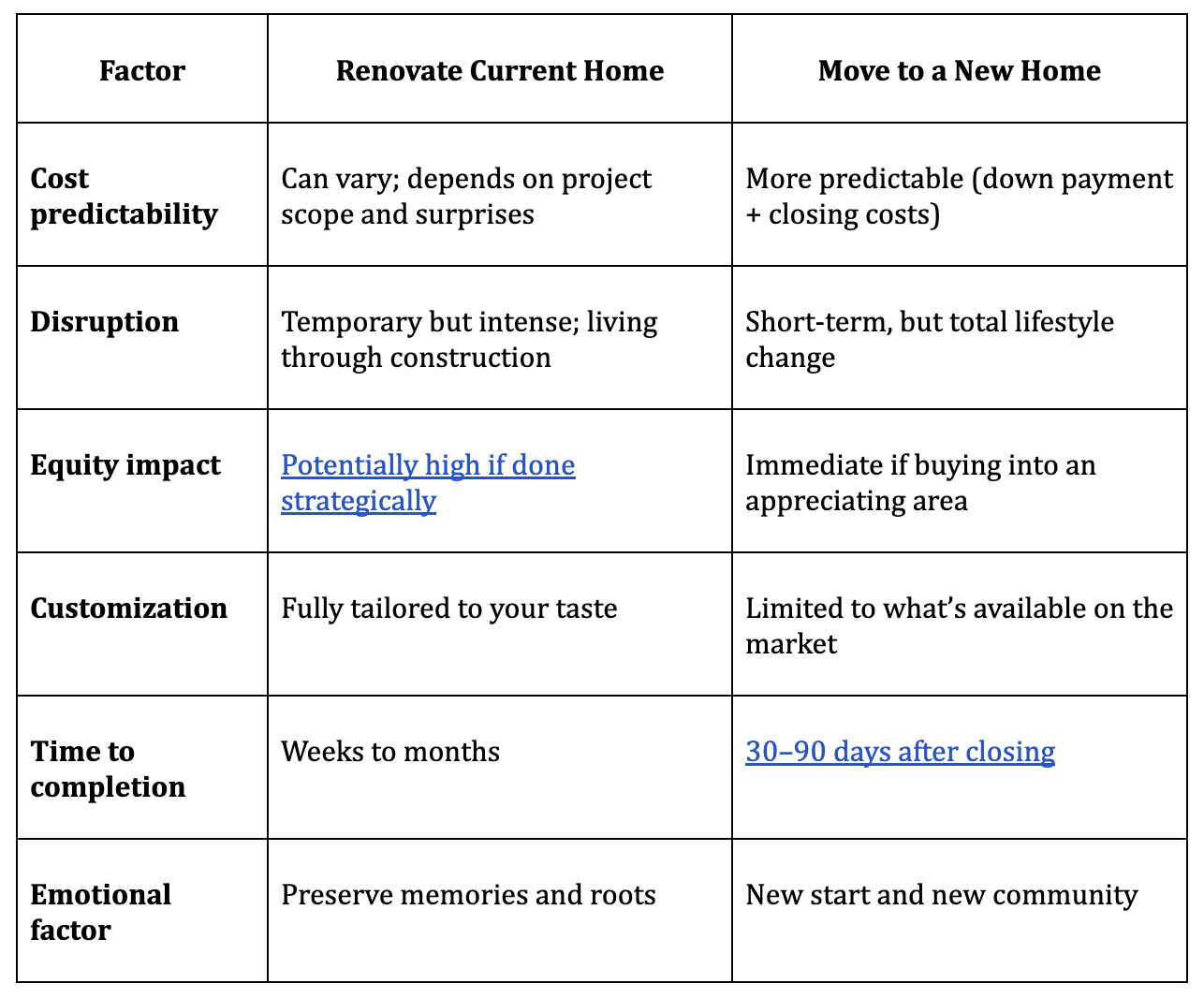

Before you commit, consider these major factors:

To help you clarify, here’s a side-by-side breakdown:

A HELOC (Home Equity Line of Credit) can make renovating financially feasible without replacing your existing mortgage. A HELOC allows you to borrow against your home’s equity at generally lower interest rates than unsecured loans or credit cards. The flexibility of drawing funds only when needed — and paying interest solely on what you use — makes it ideal for phased or multi-stage renovations.

Additionally, when used for home improvement, the interest may qualify for tax advantages. For homeowners who see long-term potential in their property, a HELOC offers a strategic way to invest in livability and value simultaneously.

Before taking action, ground your decision in objective assessment rather than impulse. Here’s how to approach it methodically.

Review this homeowner’s checklist to clarify readiness and fit.

Here are the most common homeowner questions at this decision stage.

1. Will renovating always increase my home’s value?

Not necessarily. The return depends on project type, neighborhood trends, and local buyer preferences. Over-customizing or over-improving can actually limit resale potential.

2. How do I decide between using savings, a personal loan, or a HELOC?

A HELOC typically offers the best flexibility and lower rates for home-related improvements. However, if you plan a quick sale post-renovation, cash or short-term financing may be better to avoid long-term debt.

3. What are the hidden costs of moving?

Beyond agent fees, expect closing costs (2–5% of the sale price), potential repairs on your current home, new furnishings, and higher property taxes in a new location.

4. Is renovating worth it if I plan to sell soon?

Minor updates (paint, fixtures, landscaping) often deliver quick returns. But major overhauls may not recoup costs unless you’re in a high-demand market.

5. Can I live in my home during renovation?

For small projects, yes. But for structural remodels, kitchen overhauls, or flooring replacement, temporary relocation often reduces stress and speeds completion.

6. How does the current interest rate environment affect my decision?

If your existing mortgage rate is significantly lower than current market rates, staying and renovating — especially through a HELOC — may be financially wiser than buying anew.

The decision to renovate or move isn’t just about walls and square footage — it’s about aligning where you live with how you want to live. Renovating deepens your investment in a familiar place; moving gives you a clean slate for new possibilities. The best path forward emerges when emotion meets analysis: balance the financial logic of your home’s future with the lived reality of what “home” truly means to you.